Guide To Singapore Double Tax Treaties

TAX TREATIES ENABLE YOU TO ACCESS RELIEF FROM DOUBLE TAXATION, EITHER BY WAY OF TAX CREDITS, TAX EXEMPTIONS OR REDUCED WITHHOLDING TAX RATES. THESE RELIEFS VARY FROM COUNTRY TO COUNTRY AND ARE DEPENDENT ON THE SPECIFIC ITEMS OF INCOME. FIND OUT MORE ABOUT SINGAPORE’S DOUBLE TAX TREATIES.

The development of international trade and multinational corporations has increased the need to scrutinise the issue of double taxation. As a company or individual looking beyond your own country for business opportunities and investments you would naturally be concerned with the problem of taxation, especially where you might have to pay taxes twice on the same income in the host country as well as in your home country. Consequently, you would seek to structure your operations to optimise your tax position and thereby reducing costs which would in turn increase your global competitiveness. This is where the relevance of Singapore’s DTAs or tax treaties comes into play.

Treaty provisions are generally reciprocal (applicable to both treaty countries) and non-discriminatory i.e. you would not be in a worse-off tax position than if you were a tax resident of tax country. If there is no treaty between your country and Singapore, you may still be able to take advantage of Singapore’s unilateral tax credits.

What is Double Taxation?

Double taxation arises when two or more countries impose taxes on the same taxpayer in respect of the same taxable income or capital. In other words, the same income is being taxed twice – the country of source where the income arises and the country of residence where the income is received. To relieve taxpayers from the burden of double taxation, countries provide various types of reliefs either under their domestic tax laws or under the tax treaties they have entered into with other countries.

What is a Double Tax Agreement (DTA)?

A DTA is a bilateral agreement between two countries to avoid double taxation which may arise as a result of the application of their respective domestic tax laws.

Benefits of DTAs

- The main objective of a DTA is to provide certainty regarding when and how tax is to be imposed in the country where the income-producing activity is conducted or payment is made. As a result is defines the jurisdictional authority on cross-border transactions.

- It clearly defines the taxing right of each country.

- It seeks to prevent international tax evasion by sanctioning the exchange of information between the tax authorities of the contracting countries.

- It allows you to claim for relief for taxes paid overseas.

Who can benefit from DTAs?

Only residents can benefit from the application of the DTA. A resident is defined under Section 2 of the Singapore Income Tax Act as:

- An individual: A person who, in the year preceding the year of assessment, resides in Singapore except for such temporary absences therefrom as may be reasonable and not inconsistent with a claim by such person to be resident in Singapore, and includes a person who is physically present or who exercises an employment (other than as a director of a company) in Singapore for 183 days or more during the year preceding the year of assessment; and

- A company or body of persons: Means a company or body of persons the control and management of whose business is exercised in Singapore.

If you earn foreign income from a treaty country, you are entitled to claim for relief under the relevant tax treaty by submitting a Certificate of Residence to the foreign country. This is proof of your Singapore tax residency. If on the other hand, you are a tax resident of a treaty country you will have to submit to the Inland Revenue Authority of Singapore, a completed Certificate of Residence from Non-Residents (Claim for relief from Singapore Income Tax Under Avoidance of Double Taxation Agreement) that is duly certified by the tax authority of the treaty country.

Types of Income Typically Covered Under the DTA

These are the types of income that are covered under the DTA:

- Income from immovable property

- Business profits

- Shipping and air transport

- Associated enterprises

- Dividends

- Interest

- Royalties and fees for technical services

- Capital gains

- Independent personal services

- Dependent personal services

- Directors’ fees

- Artistes and sports-persons

- Remuneration and pensions in respect of government service

- Non-governmental pensions and annuities

- Students and trainees

- Teachers and researchers

- Income of government

- Other income

Contents of DTAs concluded by Singapore

Although each DTA concluded by Singapore has specific terms and may differ from one country to another, there are certain key general principles of a typical DTA, as outlined below:

- Scope of the DTAis limited to tax residents of Singapore and the treaty country,

- Taxes covered by the DTAis limited to income taxes and would therefore exclude customs and excise duties.

- Definition of Permanent Establishment (“PE”): PE is a concept that features in all DTAs. The presence of a PE would generally determine whether an entity is taxable in another country. It basically means a fixed place where a business is wholly or partly carried on and may include:

- A place of management

- A branch

- An office

- A factory

- A warehouse

- A workshop

- A farm or plantation

- A mine, oil well, quarry or other place of extraction of natural resources

- A building or work site or a construction, installation or assembly project

- And without prejudice to the generality of the foregoing, a person shall be deemed to have a permanent establishment in Singapore if that person:

- Carries on supervisory activities in connection with a building or work site or a construction, installation or assembly project; or

- Has another person acting on that person’s behalf in Singapore who: (a) Has and habitually exercises an authority to conclude contracts; (b) Maintains a stock of goods or merchandise for the purpose of delivery on behalf of that person; or (c) Habitually secures orders wholly or almost wholly for that person or for such other enterprises as are controlled by that person.

- Income from immovable property, such as rental income from real estate, is usually taxed both in the country of source (where the property is situated) and country of residence of the recipient. According to Singapore DTAs, the country of residence will have to allow a credit for the tax paid in the country of source.

- Business profitswhich are not attributable to a PE are not taxable. However, if business profits are generated through a PE, the enterprise is allowed to deduct a reasonable amount of expenses attributable to that PE.

- Airline or shipping profitsderived by an enterprise of one country from the other country are entitled to either full or partial exemption. Where full exemption is provided for, this means that the air transport or shipping income will be taxed in the enterprise’s Country of Residence only.

- Dividend incomemay be taxed in the recipient’s country of residence and that the country of source (i.e. the country in which the company paying the dividend is resident) has the right to tax the dividend income. Normally the country of source would grant full or partial tax exemption or impose a reduced dividend withholding tax rate. Since Singapore adopts a one-tier corporate system it does not levy withholding tax on dividend payments. Whether they are taxable in the recipient country would depend on the domestic tax laws of that country and what the treaty specifies.

- Interest will be exempted or taxed at a reduced rate in the country in which the interest income arises (source country).

- Royalty incometax treatment varies from complete to partial exemption. An important point to note is that the definition of royalty may vary from treaty to treaty.

- Professional services incomeis normally taxed in the country of residence of the individual performing the services. When the individual has a fixed base in Singapore (office or clinic) his income from the professional services will be taxed in the same manner as his business profits. Professional services cover physicians, lawyers, engineers, architects, dentists, accountants, etc. Some tax treaties provide tax exemption if the individual is present in Singapore for less than 183 days in a tax year and where the services are performed for a resident of the other contracting country.

- Income from employmentwill be taxed in Singapore if the employment is exercised in Singapore unless: a. the employee is not present in Singapore for more than 183 days in a tax year b. His employer is a resident of the contracting country c. His remuneration is not borne by a permanent establishment in Singapore of an enterprise of a contracting country.Certain tax treaties also impose an additional condition to be fulfilled – the employee’s income must be subject to tax in the other contracting country.

- The source of directors’ feesis in the country in which the company paying the fee is tax resident. The full domestic tax rate would generally apply.

- Government service payments– Any salary, wage, pension, or similar rewards for personal services paid by the government of a contracting country to persons performing services in Singapore on behalf of that government are exempt from tax in Singapore and will only be taxed in the contracting country.

- Remuneration paid to visiting professors or teachers, by a contracting country, for teaching at a Singapore based educational institute is exempt from tax in Singapore.

- Self-employed personsare liable to Singapore income tax on the full amount of their income which is earned in Singapore, net of any tax-deductible expenses which they might have incurred in order to earn that income

- The right to tax capital gainsarising from the sale of immovable property and gains from sale of shares varies from DTAs signed with different countries.

- Tax credit: Singapore will give a tax credit in respect of the foreign income based on the lower of Singapore tax payable or foreign tax paid. In addition, foreign-sourced income is also tax exempt in Singapore subject to two conditions – that in the year the income is received in Singapore, the headline tax rate (i.e. highest corporate tax rate) of the foreign jurisdiction from which the income is received is at least 15% and that the foreign income has been subjected to tax in the foreign country.

Methods of Relieving Double Taxation in Singapore

The methods of relieving double taxation are given either under a country’s domestic tax laws or under the tax treaty. The available methods in Singapore are as follows:

Tax Credit

A tax credit will be given for the foreign tax suffered by a tax payer against his domestic tax imposed on the same income. The amount of tax credit relief is normally restricted to the lower of the paid/payable in the foreign and home country. This is known as the ordinary credit method vis-a-vis the full credit method, where the tax paid in the country of source is allowed as a credit in full.

Tax credit relief is commonly referred to as Double Tax Relief (“DTR”) in Singapore. The claim for DTR should be made while filing annual income tax returns (Form C) and should be shown in the company’s tax computation. Documentary proof (e.g. withholding tax receipts, letter from the foreign tax authority, or dividend vouchers) to show that the remitted income has been subjected to tax in the treaty country is required, before DTR claims can be considered.

Tax Exemption

Double taxation can be avoided when foreign income is exempt from domestic tax. The exemption may be given on the entire or part of the foreign income.

Tax Exemption for Foreign-Sourced Dividends, Branch Profits, and Service Income – Section 13(8) of the Singapore Income Tax Act

A Singapore tax resident company can enjoy tax exemption on its foreign-sourced dividends, foreign branch profits, and foreign-sourced service income that is remitted into Singapore if the following conditions are met:

- The highest corporate tax rate (headline tax rate) of the foreign country from which the income was received is at least 15% and

- The foreign income had been subjected to tax in the foreign country from which they were received. The rate at which the foreign income was taxed can be different from the headline tax rate.

Furthermore, tax exemption will be granted to all foreign sourced income earned/accrued outside Singapore to resident non-individuals and resident partners of partnerships in Singapore.

To enjoy the tax exemption on the specified foreign income, you need not submit documents (such as dividend vouchers, notices of assessment issued by the relevant foreign jurisdiction etc) with your income tax returns to substantiate that their specified foreign income qualifies for the exemption. Instead you only need to declare in the appropriate section of your income tax returns that your specified foreign income qualifies for the tax exemption and furnish the following particulars:

- Nature and amount of income (i.e. foreign-sourced dividend, foreign branch profits or foreign-sourced service income)

- Country from which the income is received

- Headline tax rate of the country from which the income is received and

- Amount of foreign tax paid/payable in the country from which the income is received.

Tax Exemptions for Individuals – Section 13(7A) of the Singapore Income Tax Act

For tax resident individuals in Singapore, all foreign income received in Singapore will be exempt from tax if the Comptroller is satisfied that the tax exemption is beneficial to the individuals.

Reduced Tax Rate

Under this form of relief, income is taxed at a lower rate and is applicable to the following classes of income: interest, dividends, royalties and profits from international shipping and air transport.

Relief by Deduction

In this case, domestic tax is applied on the foreign income after deducting foreign tax suffered. Singapore does not allow a deduction of foreign income tax. However a deduction is given indirectly as under the remittance basis, Singapore would tax the amount of foreign income received (i.e. net of foreign tax) in Singapore.

Tax Sparing Credit

Under a DTA, tax credit is usually available in the country of residence only if the income has been taxed in the country of source. Tax sparing credit is a special form of credit whereby the country of residence agrees to give a credit of the tax which would have been paid in the country of source but was not, i.e., “spared”, under special laws in that country to promote economic development.

The tax sparing credit provision is usually found in DTAs between a developing country which offers tax incentives to attract foreign investment and a developed country which is capital exporting. The credit is given by the capital-exporting country under its laws to promote investments.

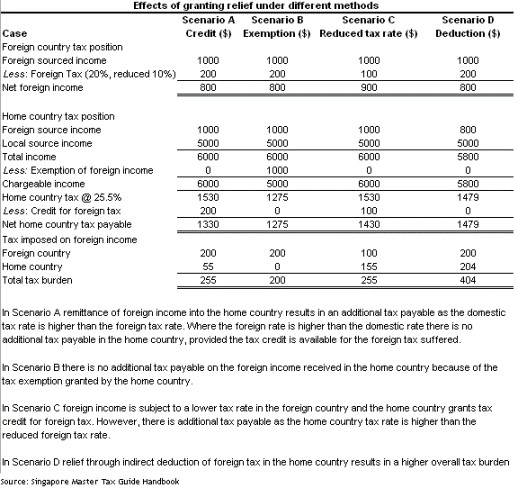

Tax Relief Example Under Different Methods

Withholding Tax

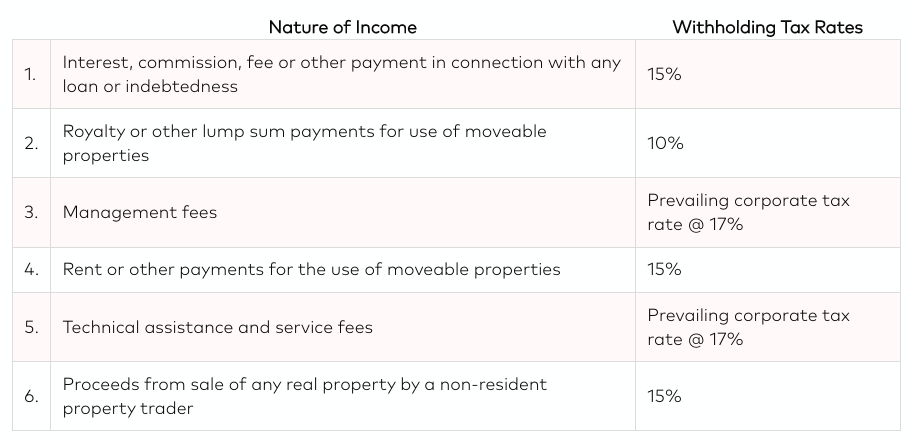

DTAs are most commonly used to determine whether it would be possible to obtain either a reduction or exemption of tax on certain types of income.

Generally, the following income is subject to withholding tax in Singapore:

Singapore’s Tax Treaty Network

All the DTAs concluded by Singapore since 1965 to date are categorised as follows:

- Comprehensive – These agreements generally cover all types of income.

- Limited – These agreements cover only income from shipping and/or air transport.

- Treaties which have been signed but not ratified – These are either comprehensive agreements or limited treaties which do not have the force of law as yet.

More questions? Let us guide you further